The Missing Page Two

PART ONE: A General Superintendent who said he would not intervene. A vote decided by a single ballot. An audit page that was not presented. A 2025 financial loss still not fully disclosed. A report involving a registered sex offender that did not result in action at the time.

One question every minister should ask before walking into the next South Texas District Council: “If everything has been handled correctly, what independent process are you willing to submit to so the body can see that?”

By Ron Bloomingkemper, Jr. | May 3rd, 2026

IN BRIEF

Former elected district officials describe events from 2008 to 2013, including the McAllen warning, a year-end loan transaction, the Executive Presbytery vote to remove Tim Barker that was later reversed, and the 2013 District Council meeting in which page two of the BKD audit report was not presented.

This piece follows a consistent approach described by multiple sources: handling matters internally and limiting outside review, across more than a decade and into the 2025 financial misconduct reported within the network’s accounting office, with estimates reaching up to $400,000.

As the South Texas Ministry Network approaches its 2026 annual conference, ministers, pastors, and members of the Assemblies of God have reason to examine what former district officials say occurred during that earlier period—and how those decisions continue to shape current questions.

Are these isolated incidents, or do they reflect a broader pattern?

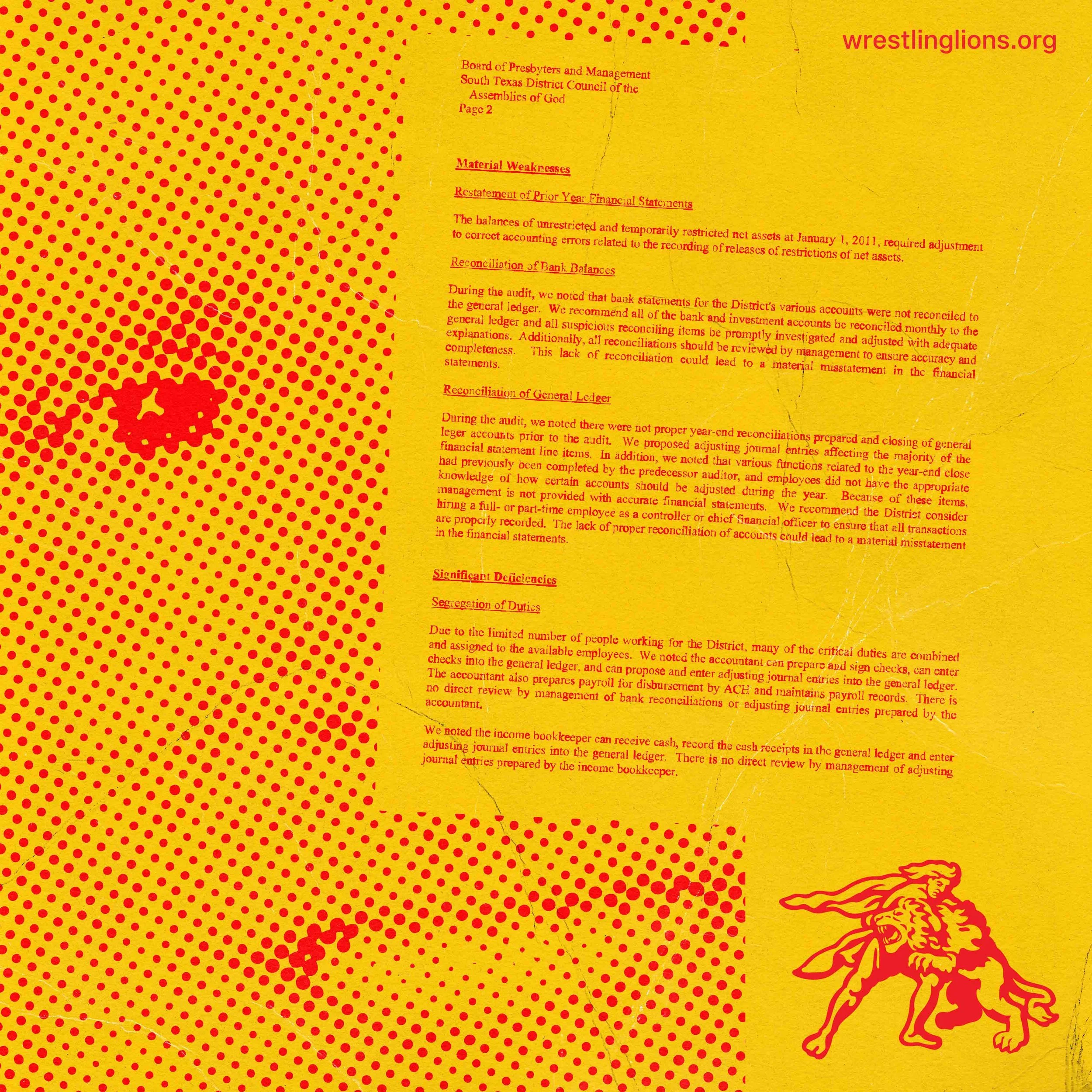

The Page That Was Skipped

April 2013. Corpus Christi.

Several hundred credentialed ministers sat in the room as Don Wiehe, South Texas District Assemblies of God Secretary-Treasurer, presented the district’s annual financial report.

He read page one. He read page three. He read page four. He read page five.

Page two was omitted.

Page two of the BKD auditors' report contained a finding that the body deserved to hear.

The auditor had identified a material weakness in the district's internal controls:

One accountant could prepare and sign checks,

Maintain payroll records, and

Enter adjusting journal entries into the general ledger with no management review.

The auditor recommended, in writing, that the district hire a controller or chief financial officer to provide independent oversight.

Download: Read the Full 2012 BKD auditor report PDF

The page that was not presented is now central to the story.

But page two was never the only thing being kept from the body. A skipped page is not just a missing detail. It’s a decision.

BKD auditors page 2 shows significant deficiencies.

Download: BKD Financial Statement Facts

But the consequences of that page did not stay in the room.

The Position He Should Never Have Held

McAllen. Tomball. Now Up to $400,000.

What the body that elected Tim Barker did not know was that, on November 4, 2008, the Board of Deacons of First Assembly of God McAllen, by unanimous consent, sent a letter to Superintendent Joe Granberry.

Along with the letter, Granberry received a packet of bank statements, credit card records, and canceled checks documenting Barker's financial conduct as their pastor. According to former district officials, no action was taken at that time.

The credit card statements were itemized by Barker himself: charges marked "T" were personal expenses, charges marked "C" were church-related. (See the detailed 62-page document below)

The letter from McAllen to Joseph Granberry asking that if Tim Barker’s name be placed for nomination as Secretary Treasurer the Executive Presbyters take into account expressed concern.

Multiple sources connected to First Assembly of God McAllen state that Tim Barker left the church owing money, with figures cited in the $32,000 range. Former district officials say they are aware of claims that money remained unpaid, but have not independently confirmed a specific amount.

“I want to know if you’d adjust my expense account. July through November and send $500 with credit card to pay off this remaining bill. (forge if needed)….. Thanks Tim Barker

Between his time in McAllen and his election to the district office, Barker briefly pastored Tomball Assembly of God. According to the same source, which identifies this information as secondhand, there were also financial concerns raised during that period. That church now operates under different leadership and a different name. No current connection is alleged between the present leadership and any prior concerns.

What surfaced later raised additional questions about financial oversight during that period.

According to former Executive Presbyters, at the end of 2010, Barker, then serving as District Secretary-Treasurer, authorized the South Texas District to borrow $90,000 from Superintendent Granberry on personal credit. The loan was dated December 2010 and repaid in January 2011.

According to those accounts, the funds were not used for operational expenses. The money was entered into the books at year-end. The same amount was removed shortly after the fiscal year closed. The transaction was reportedly authorized without the knowledge or consent of the Executive Presbytery and recorded as "NP $90,000," a note payable.

In 2011, the Executive Presbytery discovered that this loan was made and repaid to improve the 2010 financial report.

The term often used for this type of activity is "window dressing," an accounting practice in which end-of-period transactions are used to present financial statements more favorably than underlying conditions warrant. In nonprofit governance, such practices raise concerns about fiduciary responsibility, particularly regarding transparency and accurate reporting.

The same individual whose financial conduct had been documented in 2008 was, two years later, involved in authorizing this year-end transaction. The relationship between these events has been cited by former officials as warranting further scrutiny.

In 2010, about a year into Tim Barker's first term as a district officer, the McAllen board again sent a copy of the letter and supporting documents, this time to an elected official on the South Texas Executive Presbytery.

The packet was taken to Alton Garrison, the Assistant General Superintendent of the Assemblies of God at the time. A meeting was held at DFW Airport. Garrison reviewed the documents and said,

“This is damning information.”

Garrison informed George Wood, the General Superintendent of the Assemblies of God (now deceased), immediately. According to a former district official, Wood responded that the General Council could not be involved at that stage and that the South Texas District Executive Presbytery would need to conduct an investigation and make a recommendation.

That is what the South Texas Executive Presbytery did.

Following the General Superintendent's instructions, they opened an internal investigation into Barker's financial conduct during his tenure at First Assembly of God McAllen.

The Executive Presbytery, according to the South Texas District Constitution and Bylaws, is responsible for all district financial business between annual councils. The Executive Presbytery traveled to McAllen to meet with the church board.

Despite Wood's stated position that the General Council would not act apart from the district's investigation, he sent James Bradford, the General Secretary of the Assemblies of God, to attend and chair the meeting in McAllen.

The McAllen board, according to one former Executive Presbyter, "had no fight in them."

Whether the McAllen board members had been threatened with a lawsuit or were simply rattled by Bradford's presence in the room, the result was the same. In the meeting, Barker stated,

“I have apologized to them, and they have accepted my apology," and the meeting was adjourned.

Tim Barker continued to serve as District Superintendent, with Don Wiehe alongside him as District Secretary-Treasurer.

The Executive Presbytery, aware of Barker's financial history at First Assembly of God McAllen and allegations that Barker misused church credit cards, began requesting detailed statements for the South Texas District credit cards. According to multiple former Executive Presbyters, Barker and Wiehe never produced those statements, despite repeated demands during the first two years of Barker's superintendency.

The Executive Presbytery later identified additional concerns, including the use of designated World Missions and U.S. Missions funds for general operating expenses, the use of "Transform America" funds for district operations rather than their intended purpose, and continued use of Waterbury Estate funds, designated for missions, for general fund expenditures.

Repayment of these funds was demanded by both the Executive Presbytery and District Presbytery, with a deadline of December 31, 2012. According to documentation reviewed for this article, repayment was not completed until March 2013.

What is not in the existing record, but is now confirmed by former district officials, is what three Executive Presbyters did days before the September 18 vote.

On September 15, 2012, three district officials met with legal counsel to determine whether they could resign from their positions. According to those present, the attorney advised that resignation would not relieve them of their fiduciary responsibility or potential liability.

They were told their only viable option was to remain in their positions and formally demand the Superintendent's resignation.

The September 18 resolution was not a power play. It was the action three men were told, by their attorney, they were legally required to take.

In September 2012, the Executive Presbytery voted 3-2 to adopt the resolution submitted by Gene Summers requesting Tim Barker's resignation as District Superintendent.

Download: September 18, 2012, Executive Presbytery Minutes signed by Don Wiehe

The September 18, 2012, resolution itself, reproduced in full with this series, is not a vague indictment. It is an itemized bill. The resolution documented multiple red flags, including unauthorized purchases, late-payment penalties, interest charges, misallocation of designated funds, and the use of district credit cards for personal expenses.

Some of the concerns in detail include:

A $7,700 lobby piano was purchased without Executive Presbytery authorization.

Approximately $8,000 in property tax penalties from late payments to ISDs and counties during the period the district office was being remodeled.

$3,981.19 in late fees on the HCC note in 2011, plus an additional $820.44 in August 2012, with the district then paying interest on the late fees themselves.

$146,000 from the 2011 sale of the Pharr property and $289,000 from the February 2012 tower lease, both of which the Executive Presbytery had agreed in writing would be designated to the wastewater treatment plant at Hill Country Camp, both of which were instead placed in the general fund and spent on operational expenditures.

Of approximately $77,000 in cash received at the April 2012 District Council for Transform America, only $32,000 had been forwarded to the General Council at the time of the resolution. The remainder had been deposited into the general fund and spent.

The resolution also recorded Barker’s admission, at an April 2012 Executive Presbytery meeting, to using a district credit card for personal purchases, noting that conducting the resolution could jeopardize the district’s tax-exempt status.

These items are documented in the September 18, 2012, resolution adopted by the Executive Presbytery.

Download: Tim Barker Resignation Request, September 18, 2012 Resolution

Barker appealed.

The appeal went to the District Presbytery, which consists of the Executive Presbytery and the Sectional Presbyters. When that meeting convened, George Wood, General Superintendent, traveled from Springfield to chair it.

The same George Wood who had said the General Council could not act without a district investigation and recommendation. The District Presbytery voted not to allow Wood to chair the meeting. Sectional Presbyter Lloyd Maddoux was called upon to chair the meeting in his place.

Wood's message to the room, by the source's account, was:

“Tim has admitted to what he did. He has asked for forgiveness. They have said they forgive him. That should end this.”

According to former district officials, the District Presbytery was not provided with the full McAllen documentation or the financial records reviewed by the Executive Presbytery.

Barker was reinstated by a one-vote margin. Maddoux cast the deciding vote.

That decision became a defining moment in the sequence of events that followed.

The Standard, When the Standard Was Applied

To juxtapose what Mr. Barker had done, comparing that to a story told by a first-hand witness, that in 2005, a young pastor in the Houston area was reported to the district by his church's board of deacons for financial misconduct.

He was a first-time pastor building a new home. He had not borrowed enough to finish it, including the light fixtures. The fixtures he wanted went on sale. He did not have the money to buy them personally. He spent $1,500 on the church's credit card. His brother loaned him the money the next day, before the church even received the bill. When the board asked, he told the truth.

The minister was fired immediately. Then-Superintendent Joe Granberry recommended to the General Council that his credentials be pulled and that he be suspended for at least one year for misappropriation of church funds.

$1,500.

Repaid the next day.

Told the truth when asked.

Credentials pulled.

One-year suspension recommended.

Three years later, that same superintendent, Mr. Granberry, received a packet of bank statements, credit card records, and canceled checks documenting Tim Barker’s financial conduct as pastor of First Assembly of God McAllen.

According to former district officials, no disciplinary action was taken.

Same category of issue. Different outcome.

That is the standard, when the standard is applied.

The system knows how to enforce accountability. The question is when it chooses to.

The Consequences of the Page That Was Skipped, Twelve Years Later

In July 2025, the South Texas Ministry Network reported financial misconduct within its accounting office.

According to a report by MinistryWatch journalist Kim Roberts, published on August 28, 2025, the network stated that a former employee had been terminated after financial irregularities were discovered.

In the official letter, Barker wrote:

"The irregularities included unauthorized salary adjustments, personal expenses charged to Network credit cards, and unapproved reimbursements lacking appropriate documentation."

The letter also stated that law enforcement had been notified and that a "thorough investigation" would be conducted.

“According to Ministry Watch, the network did not publicly disclose the total amount involved, and requests for additional details, including the identity of the investigating firm, went unanswered.”

Estimates reviewed for this article have ranged from approximately $300,000 to nearly $400,000, though no official figure has been confirmed publicly.

According to a source familiar with the district office structure, the employee involved had authority over journal entries, check preparation, and credit card use.

That structure reflects the same internal control weakness BKD identified in the 2012 audit, on the page Don Wiehe declined to read aloud at the 2013 District Council.

The auditor recommended, in writing, that the district hire a controller or chief financial officer to provide independent oversight. No such position was created. Twelve years later, one employee held the same combination of duties the auditor had warned the body about by name.

Additional questions have been raised regarding hiring practices.

A public records request has been submitted to the Houston Police Department regarding the former South Texas District employee. District leadership has been asked, in writing, whether a background check was conducted prior to the employee's hire.

District leadership has also been asked whether the former employee's identifying information matches that of an individual who appears in publicly available Harris County court records: a misdemeanor theft case filed in December 1980 that records show resulted in a guilty finding, and a second misdemeanor theft case filed in February 1989 that records show was disposed of. The names, dates of birth, and physical identifiers in those public court records are a matter of record.

No response has been received as of publication.

If the answer is that no background check was performed before placing one human being in the chair, the 2013 auditor warned the body about by name, the body is entitled to know that. If the answer is that a background check was performed and ignored, the body is entitled to know that, too. There is no third version of this answer that reflects well on anyone in the room.

MinistryWatch also reached out to the national body of the Assemblies of God for comment. The General Council's response, as reported, was:

"The General Council has no knowledge of the alleged misconduct you are referring to nor can we speak for, or on behalf of, the South Texas District which is a separate entity."

That is the same General Council whose then-Superintendent flew from Springfield to Houston in 2012 to chair the meeting that overturned the Executive Presbytery's vote to remove Tim Barker.

In 2025, when asked about the financial misconduct that occurred under the Superintendent they helped reinstate, the General Council's institutional posture is that it has no knowledge and cannot speak for South Texas, which is a separate entity.

Could this be a pattern, or a series of unrelated events?

Based on the documented record, certain patterns in how issues were addressed appear across multiple periods.

In 2013, Tim Barker stated that the auditor’s recommendations would be presented to the credentialed body at the next District Council. The audit itself reflects those recommendations. According to available accounts, portions of those findings were not presented during the 2013 report.

In a July 30, 2025, letter, Barker stated that the network was “committed to full transparency and accountability.” As of publication, responses to specific questions raised by credentialed ministers and members of the press have not been reflected in the public record.

These events raise a broader question about how financial concerns and audit findings have been communicated over time.

Across the documents reviewed, multiple instances reflect internal handling of significant issues, while the extent of external review or independent scrutiny is not fully detailed in the public record.

The timeline includes:

Financial concerns raised in McAllen

Additional concerns described during the Tomball period (not independently verified)

Documented audit findings in 2013

Reported financial misconduct in 2025

Taken together, these events span multiple years and involve recurring categories of financial oversight and control.

“Each event stands on its own record. Taken together, they present a sequence that warrants further review.”

A separate article (Part 2) examines the 2025 financial misconduct in greater detail, including a timeline assembled from public statements and social media posts by Don Wiehe.

That record raises questions about the sequence of events, what information was publicly available at different points in time, and how those disclosures aligned with the May 2025 reelection vote.

We've All Done It Sometime or Another

In that same overruling meeting, by the account of former Executive Presbyters present, a sectional presbyter defended Barker by saying, in essence, that the rest of them had done similar things. “Tim just got caught.”

A sectional presbyter, a man entrusted with the spiritual oversight of a region of churches, suggested that financial misconduct was common enough among district leadership that Barker's distinguishing failure was being caught.

According to one Executive Presbyter, after the September 2012 meetings, a former department leader for the South Texas District told the Executive Presbyter in private:

“We know it’s all true, we just don’t care.”

Following the September 2012 vote, according to sources, multiple emails were sent to pastors across the district urging ministers to take action against the Executive Presbyters who had voted to remove Barker.

According to former district officials, Jim Rion, lead pastor of Westover Hills Assembly of God in San Antonio, helped organize efforts to defend Barker. Rion, along with Sectional Presbyter Doug Roberts, convened a meeting in San Antonio where ministers were told that Executive Presbyters were “coming against” leadership.

According to those present, the message communicated in those meetings was that support for the Superintendent was expected, and that those who opposed him should be removed from leadership roles.

At the next District Council in Corpus Christi in April 2013, a man, who had been serving as both an Executive Presbyter and the General Presbyter of the South Texas District, was voted out of office. Rion was voted in to replace him.

After this Executive Presbyter was voted out, the Assistant District Superintendent walked to a microphone and resigned his position as Assistant Superintendent and as a member of the Executive Presbytery on the floor of the council.

Another presbyter, a traveling evangelist who had submitted the resolution calling for Barker’s resignation, reported receiving calls from pastors canceling previously scheduled ministry engagements. He was voted out of his position as Executive Presbyter at the 2014 District Council.

Taken together, these events describe a pattern that multiple former officials say discouraged dissent within district leadership. According to those accounts, raising concerns or challenging decisions could result in removal from leadership positions or loss of ministry opportunities.

The financial matters documented in this article—including the handling of designated funds, the use of district credit cards as recorded in the April 2012 Executive Presbytery meeting, and the 2025 misconduct in the accounting office—have not been fully addressed in public reporting.

These issues raise questions that warrant further examination by ministers, members, and, where appropriate, external authorities.

The body can decide for itself how to interpret these events.

Inside the Room: The Day Page Two Was Skipped

Don Wiehe, the South Texas Secretary-Treasurer, recorded the date of the Waterbury repayment as December 2012 in the district’s books, although the actual repayment did not occur until March 2013. According to former district officials, he insisted that the transaction be included in the district’s 2012 financial report and represented to BKD, the district’s auditor, that the repayment had been made before the December 2012 deadline.

In April 2013, the day before the District Council’s annual business meeting, the Executive Presbytery met with BKD auditors at their offices near the Galleria in Houston. According to former Executive Presbyters present, they spent the day correcting the financials Wiehe had submitted.

Multiple sources in the room report that Wiehe became visibly frustrated during the meeting, at one point angrily saying, “I am not a liar.”

BKD did not issue a finalized audit for 2013. The report distributed to the body the next day was identified by BKD as a draft. The body did not receive a completed audit.

During the presentation of the 2012 financial report, Wiehe addressed the late repayment of designated funds and revised financial figures, without disclosing that the funds had been previously disbursed or that the auditor had identified material weaknesses in internal controls.

One credentialed minister in the room, C.E. Smith, stepped to the microphone.

According to the meeting recording, Smith began carefully:

“My discussion of these things does not make me an enemy. I have some concerns, and because I do have these concerns I want these questions to be answered… I love transparency. I have to do it at my church and I believe we are trying to get there with our district.”

Smith then asked, as the recording captures, whether BKD, as a new audit firm, had included the recommended changes in its letter to the district, and what those recommendations were.

Wiehe responded.

According to the recording, he stated that the auditor’s letters were intended for management and board personnel, that recommendations had been made, and that some had been implemented and some had not. He also stated that he could not legally share those recommendations with the body.

Audit management letters are typically directed to leadership and those charged with governance.

However, the credentialed body of the South Texas District is the corporation's membership, which retained the auditor. The district’s bylaws designate that body as the ultimate authority. No specific statute has been identified that would have prohibited the disclosure of those recommendations to the body.

Tim Barker followed Wiehe’s response with a commitment. According to the recording,

Barker stated that the report’s recommendations would be addressed and that the necessary policies would be presented at the next District Council.

The auditor’s 2013 recommendation, contained in the report, was to hire a controller or chief financial officer to provide independent oversight of the segregation-of-duties weakness identified.

That commitment was made on the floor of council, in front of the assembled body.

Following Smith’s remarks, the tone in the room shifted.

According to a ballot teller who handled the nomination submissions, one ballot included Smith’s name with a drawing of a devil beside it.

Smith was not the only minister who approached the microphone. After he sat down, Sydney Woods addressed the room and criticized the Executive Presbyters who had voted to remove Barker. In his remarks, Woods stated:

"the job of the Executive Presbyters is to support the Superintendent."

That statement reflects a view that differs from the South Texas District bylaws, which assign fiduciary responsibility for financial oversight to the Executive Presbytery rather than the Superintendent.

Leaders of 501(c)(3) organizations are generally understood to operate under three fiduciary duties: care, loyalty, and obedience. These duties include oversight of financial practices, acting in the best interest of the organization, and adherence to governing documents and applicable law.

At the conclusion of the financial report, the Assistant Superintendent resigned from the floor of the meeting. By his account:

“I could not go back into the room and serve with the knowledge of all that had been said and done. To continue serving in that role without calling everything into question publicly would be to consent to their deeds.”

No additional questions were raised regarding the omitted audit findings.

A 2013 Warning About Daniel Savala, a Sworn Denial, and the Response That Never Came

The circumstances surrounding the omitted audit findings were not limited to financial matters.

In 2013, the same year Don Wiehe presented the 2012 financial report, Ron Bloomingkemper Jr., a former Chi Alpha member from Sam Houston State University, in Huntsville, Texas, contacted by phone Tim Barker to report concerns involving Daniel Savala, a registered sex offender, who was still being promoted in Chi Alpha.

By Bloomingkemper’s account, he reported that Savala had groomed him and asked him to engage in sexually inappropriate behavior around 1997. Bloomingkemper states that Barker asked questions and said he would look into the matter. In a follow-up conversation months later, Bloomingkemper was told the issue had not yet been addressed.

Bloomingkemper has stated that he later provided a sworn declaration (an affidavit) to attorneys regarding his warnings.

In the 2026 deposition of Tim Barker concerning the John Doe one and two civil case in Harris County court, Mr. Barker, under oath, stated that he has no knowledge of having a conversation with Mr. Bloomingkemper. And went so far as to say that:

“He has no knowledge of having ever had a conversation with Mr. Bloomingkemper….. and whoever states the information that I had conversation with Ron Bloomingkemper is falsifying information….. They are lying.”

The deposition of Tim Barker being questioned about Mr. Bloomingkemper.

In interviews with former district officials, Bloomingkemper asked:

“What should have been the appropriate response of his phone call?”

One former district official described what he says he would have done

“I would have contacted the Harris County District Attorney before my next appointment. I would have called Eli Gautreaux and asked him, within 24 hours, to come to my office and bring Savala with him. I would have handled that before anything else.”

The same official was also asked about ministers who, according to court documents and survivor testimony, wrote letters to an Alaska judge requesting leniency for Savala and participated in fundraising efforts reported to total approximately $50,000.

His response:

"I would have fired everybody who sent a letter."

Court records and documented correspondence identify Eli Gautreaux, then Texas and New Mexico Area Director for Chi Alpha, and Eli Stewart, then campus pastor at Texas A&M and lead pastor of Mountain Valley Fellowship Church, among those who supported Savala through letters or related efforts.

Both men have since been removed from their ministry positions and have lost their Assemblies of God credentials. Public records indicate Stewart has relocated out of state. A complete list of individuals involved in the letter-writing and fundraising efforts has not been publicly released.

The former district official referenced Gautreaux specifically when describing his hypothetical response:

“I would have asked, did you know that Daniel was a registered sex offender when you took people to his house or encouraged others to go? If the answer was yes, I would have terminated him immediately.”

According to Bloomingkemper’s account, the 2013 report to Tim Barker, Superintendent, did not result in immediate action.

Gautreaux was later removed from his position and credentials, along with Stewart, following subsequent developments documented in court proceedings and public reporting.

The 2013 report, the earlier McAllen documentation, and the audit findings were all received within the same leadership structure.

The relationship between those events, as described by multiple sources, raises questions about how concerns were evaluated and acted upon during that period.

Same Instinct. New Victims. Same Outcome.

This is not limited to financial matters.

Across multiple incidents—financial oversight, abuse reporting, and internal investigations—former officials, survivors, and documented records describe a similar approach: issues handled internally, limited disclosure, and resistance to independent review.

Elements of that approach appear in the Daniel Savala case, in litigation currently moving through the courts in Harris County, and in accounts from multiple survivors whose experiences have been described in similar terms.

The Foley & Lardner law firm, retained by the district to conduct an investigation, has been described by survivors and credentialed ministers as operating more like defense counsel than a neutral fact-finder. According to those accounts, the investigation focused on identifying grounds for disciplinary action against individuals rather than examining broader systemic issues.

Testimony from the North Texas proceedings, including statements from Anthony Scoma, has also raised questions about the use of nondisclosure agreements and their impact on communication between survivors.

Records referenced in this series include:

A 2018 email exchange in which concerns were repeatedly raised with both National Chi Alpha and Assemblies of God leadership

According to those records, these concerns were raised multiple times over an extended period.

Each of these events stands on its own.

Taken together, they present a consistent sequence: concerns raised, internal handling, and limited public disclosure.

The record is established. The response to it is.

Thirteen Questions for the 2026 South Texas District Council

The following are questions credentialed ministers and laypeople have every right, and arguably every obligation, to bring to the floor of the upcoming South Texas District Council Conference:

Audit Transparency

Was a complete annual financial audit presented to the body this year? If not, when will it be?Independent Review

Will the district commit to an independent forensic audit conducted by a firm with no prior relationship to district leadership?McAllen Documents

Will the district release the full McAllen documentation from 2008 and 2010, with only sensitive personal information redacted?2013 Audit Record

Will the district release the full 2013 audit report, including all pages, along with the recording of that business meeting?Follow-Through on 2013 Commitments

What specific audit recommendations from 2013 were presented to the body, and what policies were implemented as a result?Internal Controls

What changes were made to address the internal control weaknesses identified in 2013, and when were those changes implemented?2010 Financial Transaction

Can the district provide a clear accounting of the $90,000 year-end loan recorded in 2010, including how it was approved and reported?2012 Decision Process

What information was provided to the District Presbytery during the 2012 appeal process, and how was the final decision reached?Savala-Related Actions

Will the district provide a complete accounting of how ministers who supported Daniel Savala were evaluated and of the actions taken? Will you release the findings of the Foley and Lardner Law firm investigation?Investigation Scope

Was the Foley law firm engaged as an independent investigator, and will the district release the scope and terms of that engagement?Abuse Reporting Protocols

What formal protocol existed for handling abuse reports in 2013, and what protocol is in place today?2025 Financial Misconduct

What is the confirmed dollar amount involved in the 2025 misconduct? Who is conducting the investigation, and what safeguards have been implemented since? Was there an arrest?Leadership Accountability

What steps is current leadership willing to take to ensure independent review and restore confidence in oversight going forward?

The Version We Don't Get to Live In

There is a version of this story in which Tim Barker was not reinstated by a narrow vote in 2012.

There is a version in which George Wood did not attend an appeal he had previously indicated the General Council would not be involved in.

There is a version in which Sectional Presbyter Lloyd Maddoux did not cast the deciding vote.

There is a version in which the 2013 Savala report was escalated to law enforcement immediately.

There is a version in which the full audit findings were presented to the body.

In that version, the sequence of events may have unfolded differently. That is not the version that occurred. The record that does exist is documented. This year, 2026, the South Texas District has the opportunity to decide how it responds to that record.

A former Assistant Superintendent who witnessed these events and later resigned rather than remain silent put it this way:

The annual conference is coming.

The questions are not complicated.

The answers will define what happens next.

The RECEIPTS: Twenty Years and One Common Thread

Multiple documented events across financial oversight, audit findings, and leadership decisions. These events occurred at different times, under different circumstances, and involved different types of concerns.

Download The extended Timeline>

What follows is a chronological record drawn from primary documents, audit reports, meeting minutes, and statements described in testimony.

This timeline is presented to allow readers to review the sequence of events and reach their own conclusions.

2005 | Tim Barker, while pastor of First Assembly of God McAllen, writes a $2,000 check from the church operating account to his own pastoral expense account without authorization. (McAllen letter, 2008)

2007 | Barker resigns from McAllen with a personal debt on the church credit card "in excess of $4,000," which the deacon board had no choice but to forgive. (McAllen letter, 2008)

2008 | The McAllen church board sends a written warning to Superintendent Joseph Granberry. The letter is reportedly never given to the Executive Presbytery. (McAllen letter, 2008; EP resolution, 2012)

2009 | Barker is elected Secretary-Treasurer of the South Texas District. The body that elected him does not know the McAllen letter exists. (Public record; EP resolution, 2012)

2011 | Barker is elected Superintendent. The McAllen church board's letter again surfaces. The Executive Presbytery travels to McAllen to investigate. James Bradford, General Secretary of the Assemblies of God, attends the meeting despite General Superintendent George Wood's prior statement that the General Council would not be involved. The McAllen board, by the contemporaneous account of officers present, "had no fight in them." (Multiple corroborating accounts)

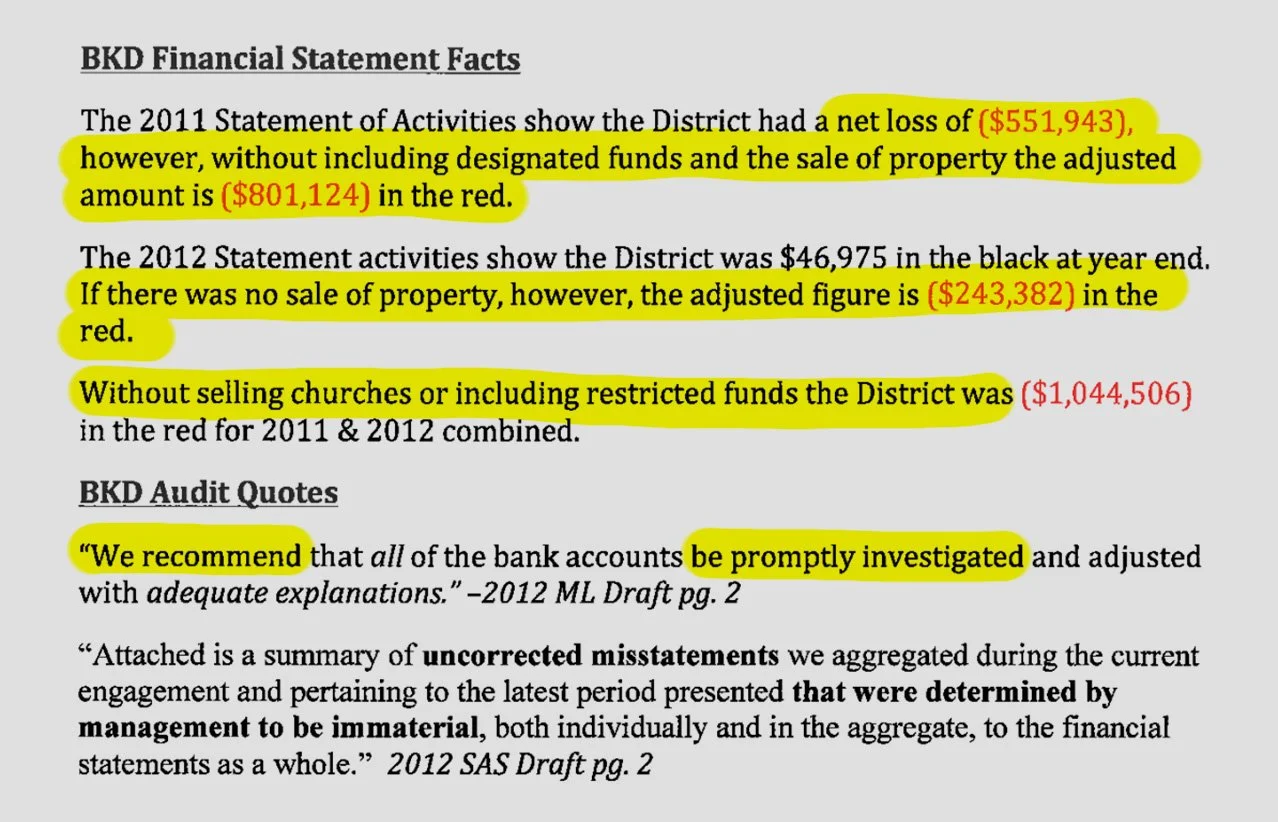

2011-2012 | The South Texas District operates at a combined loss of approximately $1.04 million, excluding property sales and restricted funds. Property is sold to cover operational expenses, in apparent violation of the Executive Presbytery's October 2011 designation of those proceeds. (BKD audit, 2013; EP resolution, 2012)

September 18, 2012 | The Executive Presbytery votes 3-2 to remove Tim Barker as superintendent on the grounds of financial misconduct, including the unauthorized use of district credit cards, which he himself admitted to in the April 2012 meeting. Don Wiehe ties his own position to the vote. The resolution and the official minutes of the meeting are signed by Wiehe. (EP minutes, 2012)

September 20, 2012 | George Wood travels to Houston to chair the emergency District Presbytery meeting, despite his earlier statement that the General Council would not be involved. The vote is overturned by a small margin. Tim Barker is reinstated. (Multiple corroborating accounts)

April 2013 | BKD's audit identifies material weaknesses in three areas, significant deficiencies in three more, twelve line items requiring proposed adjustments, no written credit card policy, no segregation of duties, and "significant difficulties" with management's cooperation. The auditor recommends hiring a controller. (BKD audit report, 2013)

April 2013 | At the District Council, Don Wiehe presents the financial report. The page containing the auditor's findings on segregation of duties and credit card policy is skipped. A member of the executive leadership resigns from the floor as Assistant Superintendent. (Witness account; documentary record now confirms the findings that were on the skipped page)

2013 | A former Chi Alpha member calls Tim Barker to report that a registered sex offender named Daniel Savala had groomed him and asked him to do something sexually inappropriate. Barker, by the survivor's account, says he will look into it and forgets. (Survivor account; Barker's own deposition, by counsel's representation, places his knowledge of Savala as early as 2010)

2018 | Donna Barrett, then General Secretary, receives a warning about Savala and forwards it to the South Texas and North Texas Districts. (Barrett's deposition, by counsel's representation in open court)

2023 | The South Texas District spends $643,910 on legal expenses in a single year, against $57,311 the prior year. (2023 financial summary, district publication)

STXD 2023 and 2024 financial statements

July 30, 2025 | Tim Barker announces that an accounts payable employee has been terminated for financial misconduct involving unauthorized salary adjustments, personal expenses on network credit cards, and unapproved reimbursements. Reports indicate the loss exceeds $300,000. The mechanisms of theft are precisely those that the 2013 BKD audit warned the Board of Presbyters were possible under the network's existing controls. (Barker letter, 2025; MinistryWatch reporting)

Through this period, the same Executive Secretary-Treasurer, Don Wiehe, has been continuously responsible for the financial oversight described above.

If the warnings were documented, the audit findings were formally presented, and similar control weaknesses were later identified in connection with reported losses…..

What actions were taken to address those risks, and when?

Notes

Quotations attributed to former district officials are drawn from recorded interviews conducted in October 2025. Documentation referenced in this series—including the 2008 McAllen letter, the September 18, 2012, Executive Presbytery resolution and minutes, the 2012 BKD audit report, and audio and video from the 2013 District Council business meeting—has been obtained from primary sources and is reproduced or directly quoted where applicable.

Reporting on the July 2025 financial misconduct disclosure draws on “Assemblies of God South TX Ministry Network Discovers Financial Misconduct” by Kim Roberts, published by MinistryWatch on August 28, 2025.

Emails were sent to Executive District leadership and the Executive Presbytery, asking for comment. We received no formal response. Any responses received in the future will be incorporated into relevant articles or appended in full.

The publisher of this series, Ron Bloomingkemper Jr., is identified in this article as the individual who reported concerns involving Daniel Savala to district leadership in 2013. He has chosen to disclose his role to provide transparency regarding his dual position as both a reporting source and the publisher of this series.